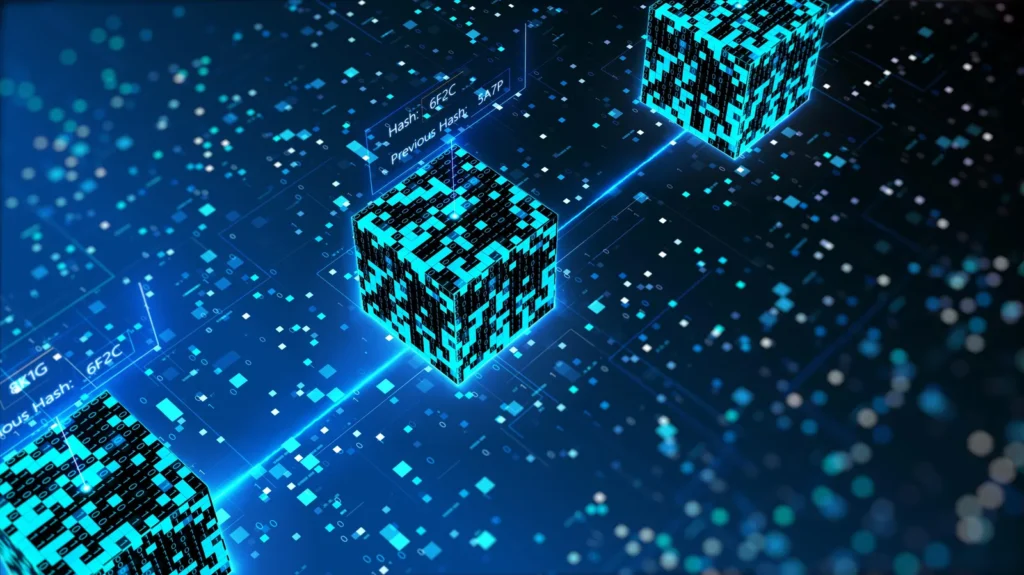

A blockchain is a special type of digital database, often called a distributed ledger, that records information in a series of connected units known as blocks. Each block stores three important pieces of information:

- A cryptographic hash of the previous block (a kind of digital fingerprint that securely links one block to another),

- A timestamp that shows when the block was created, and

- The transaction data, which is often arranged in a structure called a Merkle tree for easier verification.

Because every block is linked to the one before it, they form a continuous and secure chain — hence the name blockchain. Once data is added to a block, it’s nearly impossible to change it without altering all the following blocks and getting approval from the entire network. This design makes blockchain transactions very resistant to tampering or fraud.

Blockchains are managed by a network of computers (called nodes) that work together in a peer-to-peer (P2P) system. These nodes follow a consensus algorithm, which is a set of rules that help them agree on which new transactions are valid before adding them to the chain. Even though blockchain data can technically be changed through a process called a fork, such changes require massive coordination and are very difficult, making blockchains secure and reliable systems.

The first blockchain was created in 2008 by a person or group known as Satoshi Nakamoto as part of the digital currency Bitcoin. It was designed to act as a public ledger that records all transactions securely and transparently. Before this innovation, one of the biggest problems with digital money was double-spending — the risk that a digital coin could be spent more than once. Blockchain technology solved this issue by enabling trusted and tamper-proof transactions without relying on a central authority or bank.

Following the success of Bitcoin, blockchain technology gained global attention and inspired the development of many other cryptocurrencies and applications. Public blockchains, such as Bitcoin and Ethereum, are open systems that anyone can view, verify, and participate in, ensuring transparency and decentralization. At the same time, businesses began adopting private or permissioned blockchains, which allow only authorized users to access or manage data. While some experts have criticized private blockchains for lacking proper security or decentralization, others believe that, when designed carefully, they can be both secure and efficient — offering practical solutions for enterprise and organizational use.